Frequently Asked Questions

Your member number (ranging from 3-7 digits, zeroes not included) can be found in digital banking within any of your accounts. Check out this How-To for instructions on locating your member number, routing number, and full account number for direct deposit purposes—all in one place.

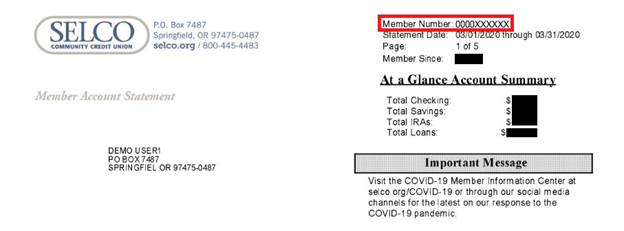

Your member number is also located in the upper right of your monthly eStatement or paper statement.

If you can't locate your member number, feel free to call us at 800-445-4483 and we'll help you look it up.

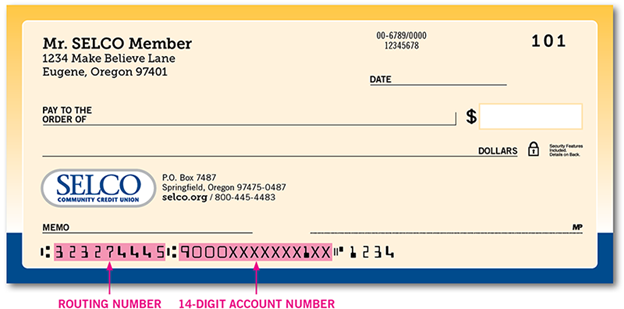

You'll need your routing and account numbers to set up direct deposit or an electronic tax refund. The routing number is the 9-digit number found in the lower left of your checks, in digital banking, and at the bottom of every selco.org page. SELCO's routing number is 323274445, which is the same for every SELCO member. Your 14-digit account number is located in the lower middle of checks, and also can be found in digital banking. Each account has a unique 14-digit account number.

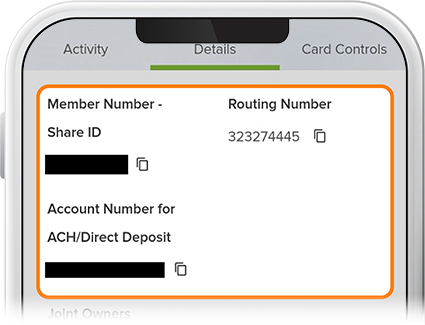

In digital banking, select any of your accounts and click or tap Details. Your member number/share ID, routing number, and full account number for ACH/direct deposits will be listed at the top. Your full account number, listed under the "Account Number for ACH/Direct Deposit" heading, will be the one you'll use when setting up direct deposit or making ACH transfers.

You can also find the routing number at the bottom of every selco.org page. Also, remember that each account has a unique 14-digit account number.